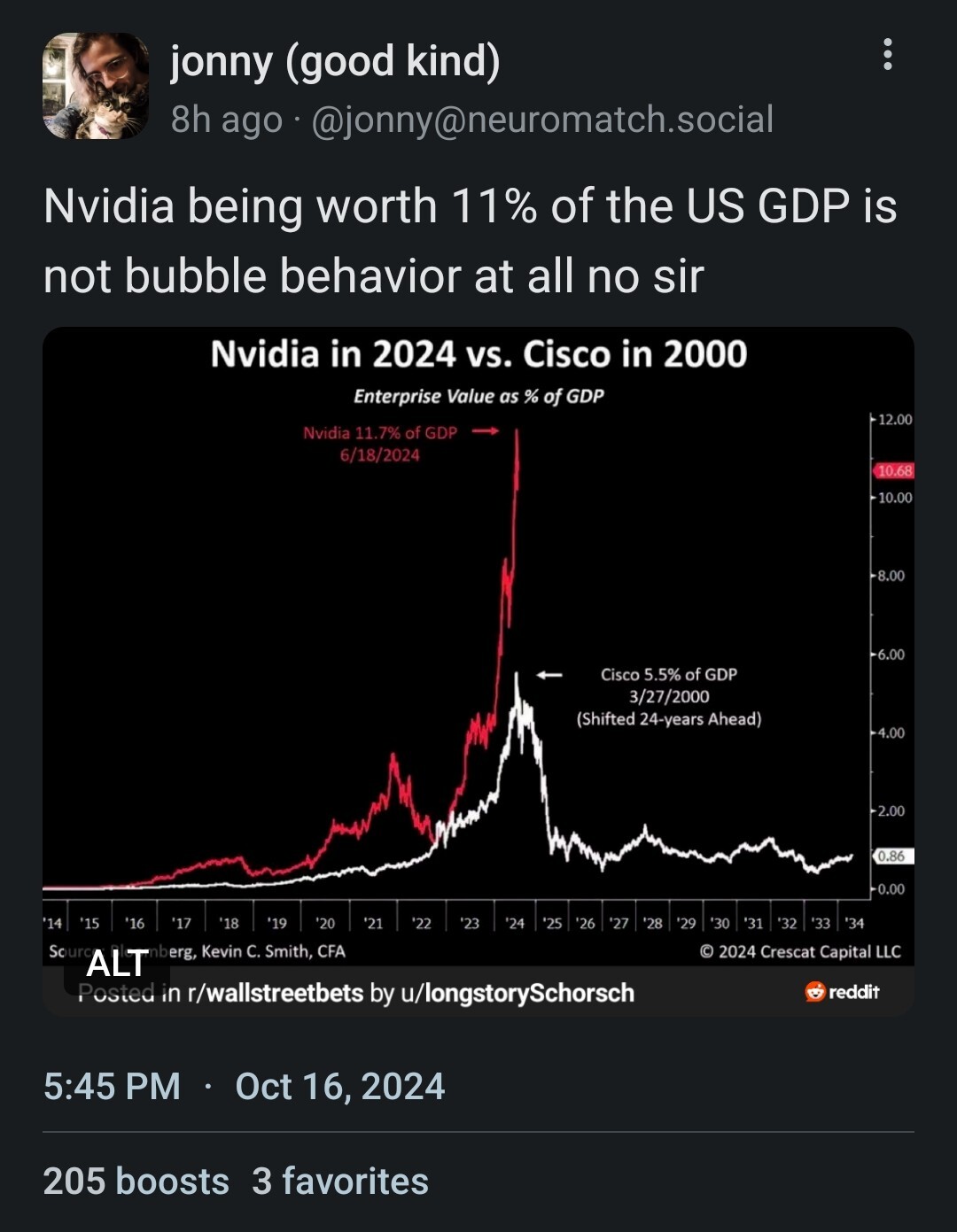

OK, here goes nothing, going to receive a roasting… TSMC is booked out to high heaven, Nvidia is completely in control of anything AI with no other company coming close to touching them, and at the end of the day, this is all but 1 month in the economy while most P/E for your average business even is near 15 or 20, corresponding to about 200 months. Cisco didn’t have a moat worth a dime and households didn’t even have always-on Internet back then, while Nvidia gets to basically set their price. Sure, AI isn’t turning out to be a great source of profit for AI providers, but Nvidia sells the shovels, not the gold or stakes of land.

Sure 11% is excessive, but I can’t see it drop like a rock any time soon. Because even if AI bursts like a bubble they are still the best at computer graphics by some margin as well, they’ll still be the best at parallel computation. And if that fails, they’re the best at making games do things, they know how to build computers and mobile devices, etc., etc. They made the Nintendo Switch for crying out loud and an RTX in my PC that I haven’t used for anything AI in ages. They’ll be fine.

And one other thing, their P/E ratio was well above 100 a bit more than a year ago. It’s at like 60 now? And the market cap doesn’t really count for anything, I mean VW was the most valuable company in the world during a short squeeze. Cisco’s P/E was apparently 200 at one point.

I think it has more to do with all that evaluation being propped up by the idea that AI will be massively profitable. All the things you mention were true five years ago when their evaluation was less ridiculous. When Nvidia’s stock evaluation falls they’ll be fine. I think the rest of the market is going to take a big hit and I expect a recession is inevitable.

Sure 11% is excessive, but I can’t see it drop like a rock any time soon.

How about when the AI pyrite rush stops? That’ll mean a hell of a lot of shovels no longer being sold. That combined with wall street expectations of never-ending growth will mean a dramatic drop when revenue is a fraction of what it was just a quarter or so ago. You’ve already pointed out that AI isn’t turning out to be a great source of profit, so it’s clearly not sustainable. All other avenues of business you mention pale in comparison to the business that AI hype brought in.

It’s also important to remember that, even if AI/ML don’t have a killer consumer application right now, those systems are really powerful for recommending targeted advertisements. That’s why all the big tech companies are throwing money at nvidia to build out more and bigger datacenters.

I don’t think the gaming market could hold them in their position if AI crashes, but they are ahead of the game on ARM as seen by the success of the Nintendo Switch.

{kind=link}

OK, here goes nothing, going to receive a roasting… TSMC is booked out to high heaven, Nvidia is completely in control of anything AI with no other company coming close to touching them, and at the end of the day, this is all but 1 month in the economy while most P/E for your average business even is near 15 or 20, corresponding to about 200 months. Cisco didn’t have a moat worth a dime and households didn’t even have always-on Internet back then, while Nvidia gets to basically set their price. Sure, AI isn’t turning out to be a great source of profit for AI providers, but Nvidia sells the shovels, not the gold or stakes of land.

Sure 11% is excessive, but I can’t see it drop like a rock any time soon. Because even if AI bursts like a bubble they are still the best at computer graphics by some margin as well, they’ll still be the best at parallel computation. And if that fails, they’re the best at making games do things, they know how to build computers and mobile devices, etc., etc. They made the Nintendo Switch for crying out loud and an RTX in my PC that I haven’t used for anything AI in ages. They’ll be fine.

And one other thing, their P/E ratio was well above 100 a bit more than a year ago. It’s at like 60 now? And the market cap doesn’t really count for anything, I mean VW was the most valuable company in the world during a short squeeze. Cisco’s P/E was apparently 200 at one point.

I think it has more to do with all that evaluation being propped up by the idea that AI will be massively profitable. All the things you mention were true five years ago when their evaluation was less ridiculous. When Nvidia’s stock evaluation falls they’ll be fine. I think the rest of the market is going to take a big hit and I expect a recession is inevitable.

How about when the AI pyrite rush stops? That’ll mean a hell of a lot of shovels no longer being sold. That combined with wall street expectations of never-ending growth will mean a dramatic drop when revenue is a fraction of what it was just a quarter or so ago. You’ve already pointed out that AI isn’t turning out to be a great source of profit, so it’s clearly not sustainable. All other avenues of business you mention pale in comparison to the business that AI hype brought in.

Totally agree with your assessment.

It’s also important to remember that, even if AI/ML don’t have a killer consumer application right now, those systems are really powerful for recommending targeted advertisements. That’s why all the big tech companies are throwing money at nvidia to build out more and bigger datacenters.

I would think that machine learning algorithms were already in use for targeted advertising from well before the AI boom.

But it’s generating the text of the ads this time.

I don’t think the gaming market could hold them in their position if AI crashes, but they are ahead of the game on ARM as seen by the success of the Nintendo Switch.